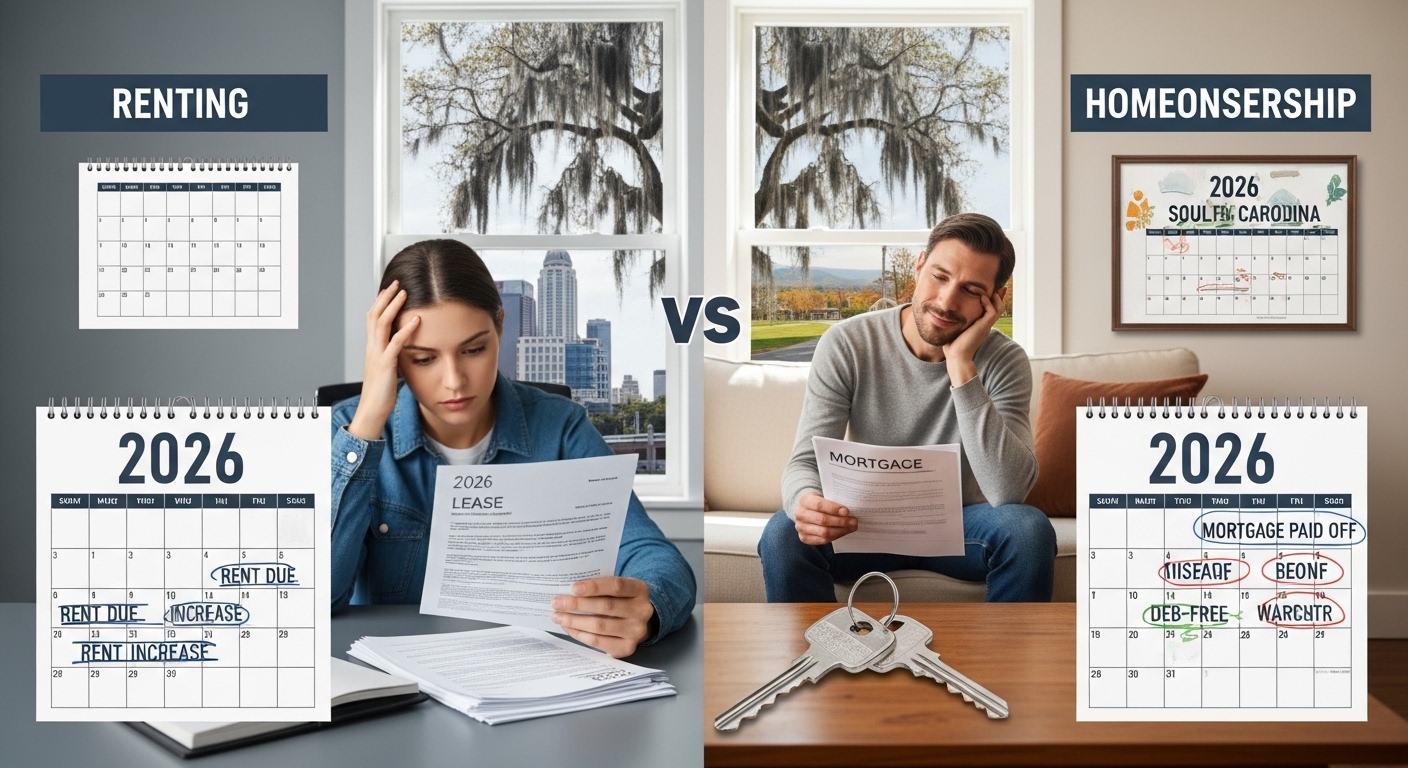

The question has been haunting renters for decades: should I keep paying rent, or is it finally time to buy? In 2026, this decision feels more pressing than ever, especially in South Carolina where the market is entering a genuinely interesting moment. I've been helping people navigate this exact crossroads for years, and I can tell you that the financial and emotional weight of this choice is real. But what's changed is that the math is actually shifting in favor of homeownership right now.

The Case for Renting (It's Still Valid)

Let me be upfront: renting absolutely has its place. Renting gives you flexibility, and it's typically easier to break a lease than it is to sell a house. If you may move in the near future, renting could be the safer financial move. This matters for people in transition, whether that's a job change, a relationship shift, or just general life uncertainty.

There's also the maintenance factor. When something breaks, your landlord usually handles maintenance. As a renter, you avoid surprise repair bills, property taxes, and major home upkeep. If you're not handy and the thought of coordinating contractors stresses you out, that's worth acknowledging.

And yes, in some markets right now, renting is genuinely cheaper month-to-month. Renting looks cheaper month-to-month in most markets today. But here's the critical thing most people miss: what looks cheaper today often costs significantly more over time.

The Real Problem with Renting Long-Term

Here's what keeps me up at night when I see people stuck in the renting cycle: your payments never stop working for someone else. You build no home equity, which means you never get a property of your own. Your monthly payment goes to your landlord. Over time, that is money not building wealth for you.

And the rent increases are no joke. Rent can also rise. Unlike a fixed mortgage payment, rent may increase every year. That can reduce financial stability. Think about what your rent could be in five, ten, or twenty years. The trajectory is usually upward, and you have almost no control over it.

Why Now Matters for Buyers in 2026

Let me cut through the noise about the current market. According to recent reporting from NAR, the average 30-year mortgage rate is projected to drop to around 6%, which is a decline from the 2025 average of 6.7%. That's movement in the right direction, and it matters for affordability.

The South Carolina market specifically is in a sweet spot right now. South Carolina's housing market is stabilizing going into 2026, with modest price movement, rising inventory, and longer days on market indicating more balanced conditions. Translation: you have more breathing room. There's less of the crazy bidding war situation we saw a few years ago, and buyers actually have negotiating power.

Here's a number that should grab your attention: it's cheaper to buy a home versus renting one in 57.7% of U.S. counties, according to Attom's Rental Affordability Report. And South Carolina trends even more favorable than the national average, especially outside of the hottest coastal markets.

The Long Game: Equity and Wealth Building

The biggest advantage of homeownership isn't about monthly payments. It's about what happens over time. While renting frees up capital for other investments, homeownership forces "automatic savings" through mortgage principal reduction. Every payment you make builds your stake in something you own.

Look at the numbers over five to ten years. Rule of thumb: If you plan to stay fewer than 3–4 years, renting is usually the better financial choice. If you plan to stay 5+ years, buying typically wins financially — especially if home values appreciate modestly. Most people aren't moving every three years. If you're thinking about staying put, the math shifts dramatically in favor of buying.

Homeownership is the primary wealth-building vehicle for most American families. The Federal Reserve's Survey of Consumer Finances consistently shows homeowners have significantly higher median net worth than renters — partly due to forced savings through mortgage payments. That's not hype. That's generations of data.

Tax Benefits You Probably Don't Realize You're Missing

One of the underrated advantages of homeownership is the tax side. Homeowners can deduct interest expenses on up to $750,000 of mortgage debt from their income taxes, though when they itemize these deductions, they forgo the standard deduction. For many people, especially early in the mortgage when interest payments are highest, this can represent real tax savings.

And here's the big one: Perhaps the best tax benefit of home ownership is receiving tax-free gains. When you sell property for a profit, it generally creates a taxable event. However if the property is your primary residence, you can exclude up to $250,000 ($500,000 for married couples) of these gains. That's massive. You're building wealth that the IRS isn't taking a cut of.

South Carolina's Market Right Now

If you're specifically looking at Easley and the surrounding area, the conditions are favorable. In March 2026, home prices in South-Carolina were up 4.1% compared to last year, selling for a median priceof $397,600. That's healthy, sustainable growth—not the bubble mentality we saw during the pandemic.

According to Rocket Mortgage, the average property tax rate in South Carolina is 0.57%. This is one of the lowest average rates in the country, higher than only five other states. If you're comparing states, that's a legitimate financial advantage that compounds over decades.

The Practical Reality: What Matters Most

All of this comes down to a few key questions you need to answer honestly:

Are you planning to stay? Purchasing a home is typically the wiser financial choice if you plan to stay there for at least five years. Over that time, you build equity and spread out your closing costs. If you expect to move sooner, renting may be cheaper. If you see yourself in the same area for five years or more, buying wins.

Is your financial situation stable? If you have a stable income, a credit score above 700, savings for a down payment, and low debt, buying is likely the right financial move. You don't need to be perfect, but you do need to be grounded.

Do you want control over your space? As a homeowner, you have the freedom to customize your living space to suit your preferences and needs. Whether it's renovating the kitchen, planting a garden, or painting the walls your favorite color, home ownership allows you to create an environment that reflects your personality and lifestyle. This level of control is often not possible in rental properties. This matters more than people think for actual happiness.

One More Thing About Your Future

Statistically and for a variety of reasons, homeowners tend to have better physical and mental health than renters, especially in the 45-64 age range. Homeowners have a lower prevalence of chronic diseases and are happier in general. There's something about ownership—real ownership—that impacts wellbeing in ways that monthly payments to a landlord never will.

The emotional side matters as much as the spreadsheet. Owning a home can foster a stronger sense of community and belonging. Homeowners tend to stay in one place longer than renters, which can lead to deeper relationships with neighbors and a greater investment in the local community. You're not just buying an asset. You're planting roots.

Making Your Move

If you're sitting on the fence about homeownership in 2026, I encourage you to stop thinking about it as one giant decision and start thinking about it as a series of small steps. Check your credit score. Talk to a lender about what you can afford. Look at homes on HOUSEJET to understand pricing in your area. Go visit some neighborhoods.

The South Carolina market is genuinely favorable right now for people who are ready to move forward. The rates are better than they were last year. The inventory is more reasonable. The prices are growing sustainably instead of jumping 20% annually. These conditions don't last forever.

I've been a real estate agent in Easley long enough to know that the people who regret their decisions aren't the ones who bought too early—they're the ones who waited too long and watched prices climb while someone else built equity in their home. Renting has its place, absolutely. But if you're financially ready, planning to stay put, and looking for something that's truly yours, 2026 is a genuinely good year to take that step.

I'm here in Easley helping people figure out exactly what that looks like for their situation. If you want to talk through the numbers specific to your circumstances, that's what I do. Let's find you the right answer for your future.